Amigoshoring’s DNA

Amigoshoring’s DNA

Supply chains move fast - let’s get ahead! Following the “three amigos” summit, we show Mexico hasn’t been a big winner from China offshoring. We also go beyond baths and ship more Mexican beer.

North American Supply Chains - USMCA Gets DNA

The annual tripartite summit between the leaders of Canada, Mexico, and the U.S. this week led to the “Declaration of North America” (DNA). That came as the USMCA dispute panel ruled against the U.S. implementation of rules of origin for autos imports from Mexico and Canada.

While nowhere near the level of ambition of the 2016 summit which led to the renegotiation of NAFTA to become USMCA, the DNA confirms that all three “seek to forge stronger regional supply chains.”

That raises the question: has Mexico been a beneficiary from reshoring away from China since the implementation of USCMA?

U.S. imports from Mexico nearly equaled those from China in November 2022 at $36.8B and $36.9B respectively. That follows a 19% increase in imports from Mexico over the last 12 months versus a year earlier, while those from China only increased by 10%. Over the past five years, imports from Mexico climbed 8% annually while those from China grew by just 2%.

Exports from China have suffered a drag from Section 301 import duties and more recently from pandemic-related disruptions. Imports from Mexico are also volatile because energy and food shipments which can face wide price shifts.

Figure 1 shows the imports from China and Mexico adjusted for import prices. On that basis, imports from Mexico are still 10% lower in real terms than those from China in November, and 25% lower over the last 12 months.

Over the longer term though there is evidence of sourcing switching away from China, as discussed in our 2023 Outlook. Mexico is not the only destination, with Vietnam being another major winner from reshoring.

Figure 2 shows the 25 products with the largest drop in U.S. imports from China in the past 12 months versus 2016. It compares the growth in imports from Vietnam to those from Mexico.

Vietnam has been the winner over Mexico in nine of the top 10 largest products and 18 of the top 25. Vietnam has seen significant wins in electronics, while Mexico has done better in industrial components and energy products.

Even in areas where Mexico has done better than Vietnam in technology, for example in solid-state devices, other countries have gained even more. Figure 3 shows U.S. imports of SSD and similar media, with South Korea, Taiwan, and Malaysia all outpacing Mexico as an alternative source from China.

Chinese exporters haven’t entirely lost out though. Figure 4 shows EU imports of SSD and similar devices. China accounted for 25% of EU imports of SSDs in the 12 months to Sept. 30, only down a little from 27% in 2016, and they are up in real terms.

South Korean exporters, who increased to a 25% share from 4% over the same period, have instead taken market share from other suppliers including those from Taiwan and the U.S.

Consumer - Beyond the Bed, Bath and Beer Peaks

Homewares retailer Bed, Bath and Beyond has reported revenues in FQ3’23 which fell by 33% year over year, while inventories fell by 25%. That has come as a result of “a period when our merchandise and strategy had veered away from (customers’) preferences.”

The wider challenges the homewares retail segment faces can be seen in the U.S. import data shown in Figure 5. In November, imported towels and bedding fell by 33% year over year, while metal implements (e.g. cutlery) and flatware fell by 35% and 24% respectively.

Home appliance manufacturer Electrolux reported a larger-than-expected loss for Q4’22 due to lower-than-expected consumer demand and the cost of cutting inventory, among other issues. The reduced demand and inventories of appliances more broadly had already been visible in U.S. government figures.

Athleisure retailer Lululemon trimmed its sales guidance for the latest quarter by 2% and cut its operating profit margin outlook. While no specific reasons have been given for the cut, it’s worth noting that supply chain activity in the athleisure sector has slowed and sourcing patterns are in flux, as discussed in our Dec. 10 report.

Fast Retailing, owner of Uniqlo, has maintained its sales guidance for the year to August 2023 of 15% year-over-year growth. Europe and the Americas are doing better than expected while Greater China is doing worse. Its GU division was particularly strong as it had a “sufficient supply of products that captured mass fashion trends.”

Abercrombie and American Eagle increased their estimates of the latest quarter sales due to prior inventory optimization (aka having the right goods in the right quantities).

U.S. beer sales are reportedly in decline as the result of higher prices. Constellation Brands have noted that “the consumer is overly sensitive to pricing actions.” Beer supply chains are a complex mix of regional brewing and international shipments of export brands.

Figure 6 shows the degree of seasonality in U.S. beer imports, as well as the 10% year-over-year decline in the volume of imports in November. That may represent a turnaround from earlier growth, with volumes having risen by 3% year-over-year over the past 12 months and by 12% compared to 2019.

Tastes are also changing. Imports of beers from Mexico climbed by 9% year-over-year in the past 12 months and by 25% compared to 2019. That gave exporters including Heineken a share of 79%. That’s come at the expense of European beers, including those from the Benelux whose share dropped to 11%.

Technology - More Money, More Problems

The government of Taiwan has passed new legislation allowing semiconductor firms to take a 25% tax credit on R&D budgets. That follows similar moves to support local investments in South Korea, the U.S., and Europe, while China is scaling back somewhat.

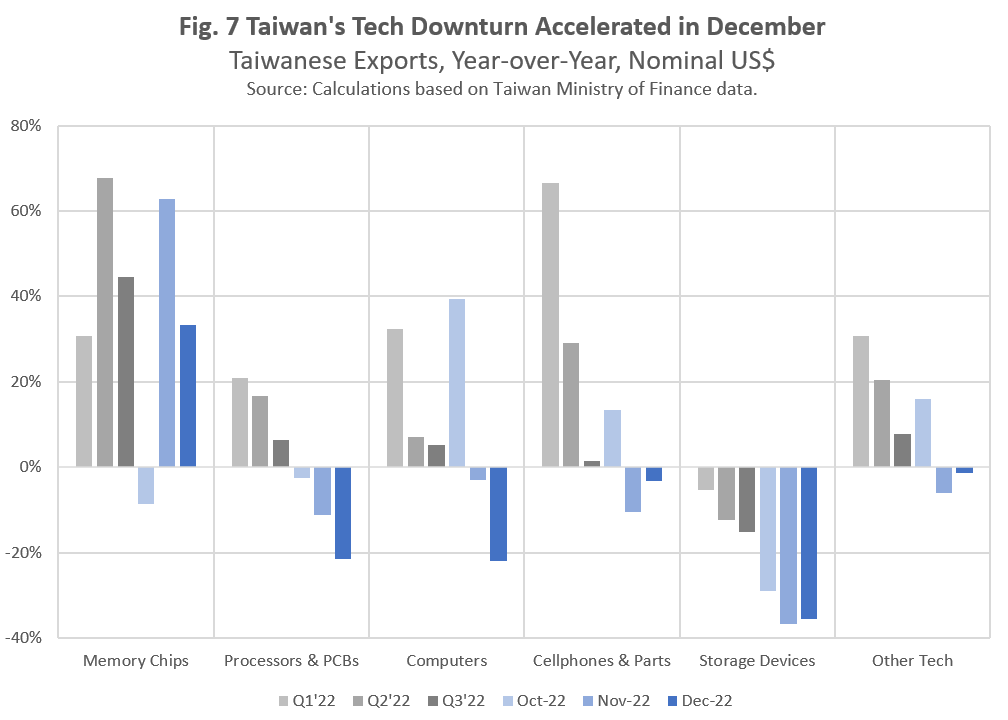

That comes as the Taiwanese authorities have cut their outlook for exports more broadly. Total December exports from Taiwan fell by 12% year-over-year, making the fourth decline after 26 months of expansion

The main driver of the drop in exports has been a decline in shipments of assembled technology products, as shown in Figure 7. Exports of computers fell by 22% in December while cell phones dipped by 3%. Among components, exports of DRAM surged by 33% but processors and storage fell by 22% and 36% respectively.

Taiwan-based chipmaker TSMC has stated its revenue in Q1’23 will face a drag from “continued end market demand softness, and customers’ further inventory adjustment.”

The U.S. is reportedly pushing its allies to restrict shipments of advanced semiconductors to China, following similar measures applied by the U.S. in October. Taiwan is not part of the discussion group.

As noted below, mainland China’s exports of semiconductors slumped 19% lower year over year in December.

Apple may extend its own semiconductor production to swap out communications chips from Qualcomm in 2024 and Broadcom in 2025. The firm may also start producing its own displays thereafter, potentially linked to the roll-out of touchscreens for its Mac line of computers. That all comes as part of a wider supply chain restructuring by the firm.

At the same time, there are signs that Apple’s remaining suppliers including BOE Technology are also reshoring their production to cut costs and reduce risk. Tata may also takeover some Indian manufacturing of the iPhone from Wistron.

Computer peripheral supplier Logitech has cut its sales guidance for the 12 months to March to a drop of 13% to 15% from 4% to 8% previously. The firm cited a “slowdown in sales to enterprise customers” as well as “uncertainty in supply availability related to the current Covid outbreak in China.”

Industrials and Commodities - Weaker Trade, Better Inventories

Chinese exports fell by 9.9% year over year in December, marking the third straight decline. Figure 8 shows that the biggest contributors to the downturn in dollar terms have been the technology and consumer goods sectors, while commodities have remained more robust.

In the technology sector - shown in orange above - exports of semiconductors fell by 16% in nominal terms and by 19% in real terms. Exports of cell phones - which have been affected by Foxconn’s manufacturing challenges - fell by 29% in nominal terms and 33% in real terms.

Refined oil exports jumped 206% higher on increased prices, though in volume terms exports climbed by 138%. The elevated demand and prices may be behind the government’s decision to increase crude oil import quotas.

Volkswagen has stated “ongoing supply chain shortages” are “expected to improve step by step in the course of the year.” A slowdown in automotive production due to a shortage of chips has been a major factor in cutting industrial inventory levels.

EU companies’ assessments of their inventory levels reached the highest since July 2020 in December. As indicated in Figure 9, the balance measure has been steadily increasing since Oct. 2021. At 9.4 in December it is well above the 10-year average of 4.0.

Export orders of -11.7 lowest were their lowest since March 2021 and have now been negative for six straight months. Industrial sentiment more broadly at -2.2 is slightly better than in November, but still close to the worst since late 2020.

The World Bank has downgraded its global GDP forecast for 2023 to a growth rate of 1.7% from 3.0% in its June forecast. That includes a 1.6% increase in world trade activity in 2023, down from 4.3% in the prior forecast.

Figure 10 shows that the Bank has steadily increased its 2022 forecast since first issuing it in January 2021, but has steadily downgraded its 2023 and 2024 outlook.

The G7 group of nations is close to defining restrictions on Russian exports of refined oil products that are due to be applied from Feb. 5. This will likely take the form of price caps, varying by product-type, applied via restrictions on shipping and insurance firms. That would be similar to the system applied in crude oil in December.

The IEA has warned that “the reconfiguration in global trade implicit in that oil product ban is going to be significantly more complex than what we have seen already” for crude oil.

The most significant impact will likely be felt by EU importers. Figure 11 shows that EU imports of refined oil products from Russia fell to 27% in September 2022 from 38% in Q2’22. A significant part of the slack has been taken up by Saudi Arabian suppliers which had a share of 17% in September.

Sweden’s state-owned mining company SKAB has discovered a 1 million-ton deposit of rare earth materials, used in high-power magnets. That may help Europe’s push for an increased share of renewables and electric vehicle manufacturing.

There are significant hurdles to production, however. The deposit itself could take a decade to develop. The processing of rare earth metals can be environmentally damaging and requires significant capital investments. It's unlikely that Sweden’s government would want to export the ore to China - the largest refiner - for processing.

Hanwha Group will reportedly invest $2.5B in an integrated solar panel manufacturing facility in Georgia, USA. Rival JA Solar also plans to open a panel plant in Arizona.

Both may allow access to Inflation Reduction Act funding and comes as U.S. authorities are cracking down on imports.

Logistics - Houston Dealing With a Problem

Port Houston will implement container dwell fees from Feb. 1 to “promote fluidity of cargo movement” after “the recent increase in demand.”

Figure 11 indicates that volumes handled by the port, on a days-adjusted basis, climbed by 17% year over year in the 12 months to Nov. 30, 2022, and by 34% compared to calendar 2019. That likely reflects west-to-east coast volume shifts as well as earlier infrastructure investments.

Another major factor has been the surge in exports, with loaded exports reaching a record high in November. Shipments of empty containers have also surged as the port attempts to clear earlier backlogs.

Elsewhere, the logistics industry is dealing with a downturn, as flagged in our 2023 Outlook. Container lines are reportedly looking to defer deliveries of new vessels in the face of falling demand.

Shipping rates for routes out of China fell by 4.3% last week, marking the 25th straight decline and leaving rates at their lowest since November 2020. They are, nonetheless, still 1.46x higher than the 2019 average and 1.89x their April 2016 trough.

The latest data from IATA shows global airfreight handling fell by 14% year over year in November 2022 and was 10% lower than in the same period of 2019.

Employment in the U.S. logistics sector was unchanged in December versus November but is now 0.7% below its August peak. The decline has been driven by a 2.1% dip in courier payrolls and a 2.5% slide in warehousing.

Disclaimer: This report is for information purposes only, not for legal, business, or financial decisions. It’s based on the latest available information on the publication date - that information may have changed by the time you read this report. Use it at your own risk.