Buzz Now, Buy Later

Buzz Now, Buy Later

Supply chains move fast - let’s get ahead! It’s CES week, so we’ve taken a look at the state of TV supply chains, semiconductor subsidies, and electric vehicle investments.

Set for Change - CES and Supply Chains

The Consumer Electronics Show in Las Vegas this week brings the usual crop of both weird-and-wonderful and mundane announcements. For many electronics retailers, creating a buzz is more important than ever as demand for devices declines in the wake of the pandemic-era splurge. So, what’s the state of consumer electronics supply chains?

There were plenty of TV and audio product announcements at CES 2023 with the usual crop of bigger and brighter screens from Sony, Samsung Electronics, LG Electronics, and TCL among others.

Exciting new products are more important than ever for retailers. Elevated sales during the COVID-19 stay-at-home spending boom are reversing. U.S. retail sales by electronics and appliance stores fell for a sixth straight month in November, with a sequential decline of 1.5%.

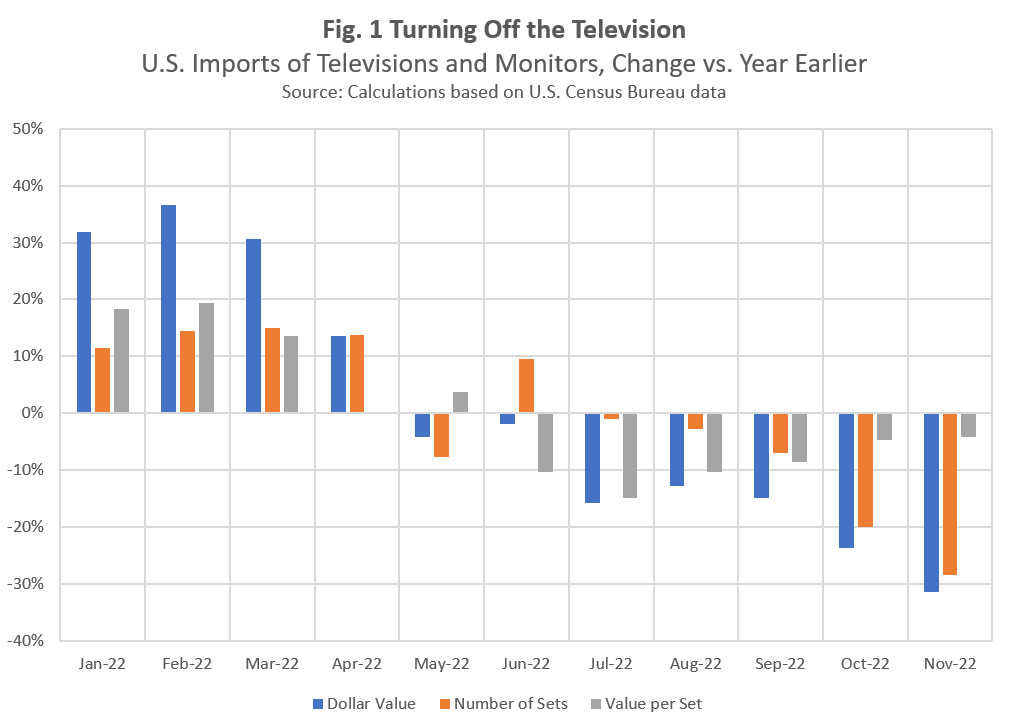

Retailers may be expecting a further decline. U.S. imports of televisions fell by 31% in dollar terms in November 2022, as shown in Figure 1, including a 28% slide in the number of units and a 4% decline in the import cost per set.

While CES may generate a buzz now, the actual deliveries of new models can come much later in the year. Figure 2 shows U.S. imports typically peak in the September to November period with a trough in Q1.

In 2022 there was a peak in Q1 as supply chains debottlenecked, while the late-year peak appears to have been sooner than normal in September. It may be much later in 2023 before we see where the underlying state of retailers’ demands ends up.

With sales in decline, retailers may also review their sourcing to look for cheaper alternatives. Figure 3 shows that the share of U.S. imports from China has fallen steadily to 54% in the 12 months to Oct. 31, 2022, from 70% in 2018. Imports from Mexico and Vietnam have compensated.

More recently there’s been an accelerated decline in shipments from China. That may reflect manufacturing woes in relation to COVID-19 which could continue in 2023. As we discussed in our 2023 outlook report, that may be a theme across the consumer electronics sector this year.

Consumer - Evidence of Early Shopping

It’s not just TVs where sales are down. Recent data shows U.S. personal consumption expenditures on goods, adjusted for inflation, fell by 0.7% sequentially in November and by 0.7% versus the same period a year earlier.

Figure 4 shows that a slowdown in spending on durable goods was the main culprit in November. Given there was a bounce in October, that may indicate earlier-than-normal shopping. A steady rise in services consumption also suggests consumers are still shifting back to pre-pandemic spending patterns.

Adobe reports that online spending during the U.S. holiday season rose by 2.5%. It’s worth noting that the figure is not adjusted for inflation, though Adobe notes a high prevalence of discounts.

There was also a sharp reversal in U.S. imports, which fell by 8% sequentially in November on a nominal (i.e. including inflation), advance basis. Figure 5 indicates that shipments of consumer goods slumped 13% lower and were 10% lower than a year earlier - the first time they have fallen on that basis since August 2020.

U.S. tariffs on imports of baby milk formula have been reimposed. Temporary relief had been provided in 2022 due to a domestic production shortfall. Imports reached a record $45M in November 2022 and averaged $38M per month since July, according to U.S. Census Bureau data, while in 2021 before the tariffs were cut imports averaged just $7M per month.

Technology - Chips are Down, Subsidies are Up

The South Korean government reportedly plans to implement larger tax breaks for investments in semiconductor manufacturing equipment. That follows the U.S. Chips for America Act and similar moves by the EU and Japan to encourage investment in the next generation of semiconductor fabs.

South Korea’s exports of semiconductors, shown in Figure 6, fell by 26% year over year in Q4’22 and were just 15% above Q1’19 levels. There’s a similar picture for OLED screens and microchip packaging which fell by 12% and 47% respectively in Q4’22 versus a year earlier.

Communications chipmaker Qualcomm has indicated that “there is significant inventory for some of our customers” and that it could take “a couple of quarters is what we think it takes for it to get to a better place.”

The Chinese government is reportedly changing tack and is deemphasizing investment in subsidizing new facilities in favor of operational measures such as cutting materials costs.

Computer-maker Dell plans to “meaningfully lower” its use of chips that are made in China, and phase them out altogether by 2024.

Foxconn’s iPhone manufacturing in China by Foxconn has reportedly returned to 90% of capacity. That follows COVID-related staff shortages in late 2022. The hold-ups may contribute to Apple’s reported plans to (a) shift production to another country and (b) use Luxshare for some production of the iPhone Pro model in China.

The impact of the shortfall in production can be seen in U.S. imports of phones. Total imports, shown in Figure 7, fell by 36% year over year in November after a 7% slide in October, based on U.S. Census Bureau data.

Autos - Loss of Traction

Japan’s big seven automakers suffered a production setback in November, with global production down by 5% year over year and down by 12% versus 2019, according to company filings. Production in Japan was more robust, up by 2% year over year but still down by 6% compared to 2019.

South Korean autos exports increased by 28% year over year in December in dollar terms, and at $5.4B they reached the highest one-month value on record. The global picture is less bright, with exports of car parts down by 6%, the first drop on that basis since June.

U.S. production of autos fell by 11% sequentially in November on a seasonally adjusted basis, potentially reflecting continued supply chain challenges. That likely held back sales, which fell by 16% in December and dragged total auto sales down by 6%.

Tesla missed analysts’ expectations for new vehicle deliveries in Q4’22, blaming logistics bottlenecks. Production in China has also been restricted because of COVID-19.

The shift to electric vehicles can be seen in U.K. vehicle registration data for 2022. Total deliveries fell by 2% year over year, while electric vehicles climbed 40% to overtake diesel.

Stellantis has warned that the rising vehicle prices, particularly for electric vehicles, could lead to a reduction in manufacturing capacity in the sector. The firm’s CEO estimates it costs 40% more to produce an EV than a combustion-engine vehicle.

The U.S. government may have found a route to cutting controversy with its allies over electric vehicle subsidies provided under the Inflation Reduction Act. New guidance indicates commercially leased cars from countries with which the U.S. has a trade agreement may be eligible. The question of the treatment components, especially batteries, remains unaddressed.

The move to electric vehicles is also leading to a range of unorthodox new partnerships. Several were detailed at CES including Nvidia with Foxconn, LG with Magna as well as Sony’s Afeela electric vehicle with Honda.

Industrials and Commodities - Less Activity, Cheaper Gas

U.S. manufacturing activity fell to its lowest since May 2020, according to the latest ISM survey. That included marked declines in new orders, including both export and import orders.

As shown in Figure 9 above, that comes as China’s activity improved, according to the CFLP survey, though China’s export and import orders also fell. While not directly comparable, China’s ratio of 50.3 (over 50 indicates expansion) was better than the United States’ 48.4 for the first time since May 2020.

Manufacturing is in decline more broadly, according to S&P Global’s proprietary measure, with the index in contractionary territory for a fifth straight month.

Australia’s government has indicated that there will be “big pressure on the Chinese workforce, big pressure on supply chains” as a result of China’s revised COVID-19 measures.

European natural gas prices have started 2023 on a downward trajectory. That partly reflects warm weather, but also reflects a range of new gas sourcing deals and the return to operation of a key pipeline.

European buyers nonetheless face competition from major Asian consumers. While gas prices are close to the level seen at the start of the war in Ukraine, they are still well above historic levels.

The Chinese government has increased its export quotas for refined oil products by 46% year over year. That may be part of attempts to reflate the economy as well as a return to historic levels. Exports had previously been restricted in the face of higher global prices, in an attempt to suppress domestic fuel costs.

Figure 10 shows that exports of refined oil products had already improved in November, having increased by 47% year over year to the highest since June 2023.

The Chinese government has also approved the import of coal from Australia. Supplies had previously been curtailed due to a spat around Australia’s criticism of Chinese labor practices.

Container shipping rates for routes out of China fell for their 26th week to Jan. 6. Rates are now 65% below their peak, and are their lowest since November 2020. They are nonetheless still 1.5x their 2019 level.

Notably, China-to-U.S. west coast rates are 1.22x their 2019 level while China-to-U.S. east coast is 1.54x the 2019 level. That may reflect ongoing diversions of traffic as shippers remain wary of the risk of a strike during wage negotiations on the west coast in 2023.

Disclaimer: This report is for information purposes only, not for legal, business, or financial decisions. It’s based on the latest available information on the publication date - that information may have changed by the time you read this report. Use it at your own risk.